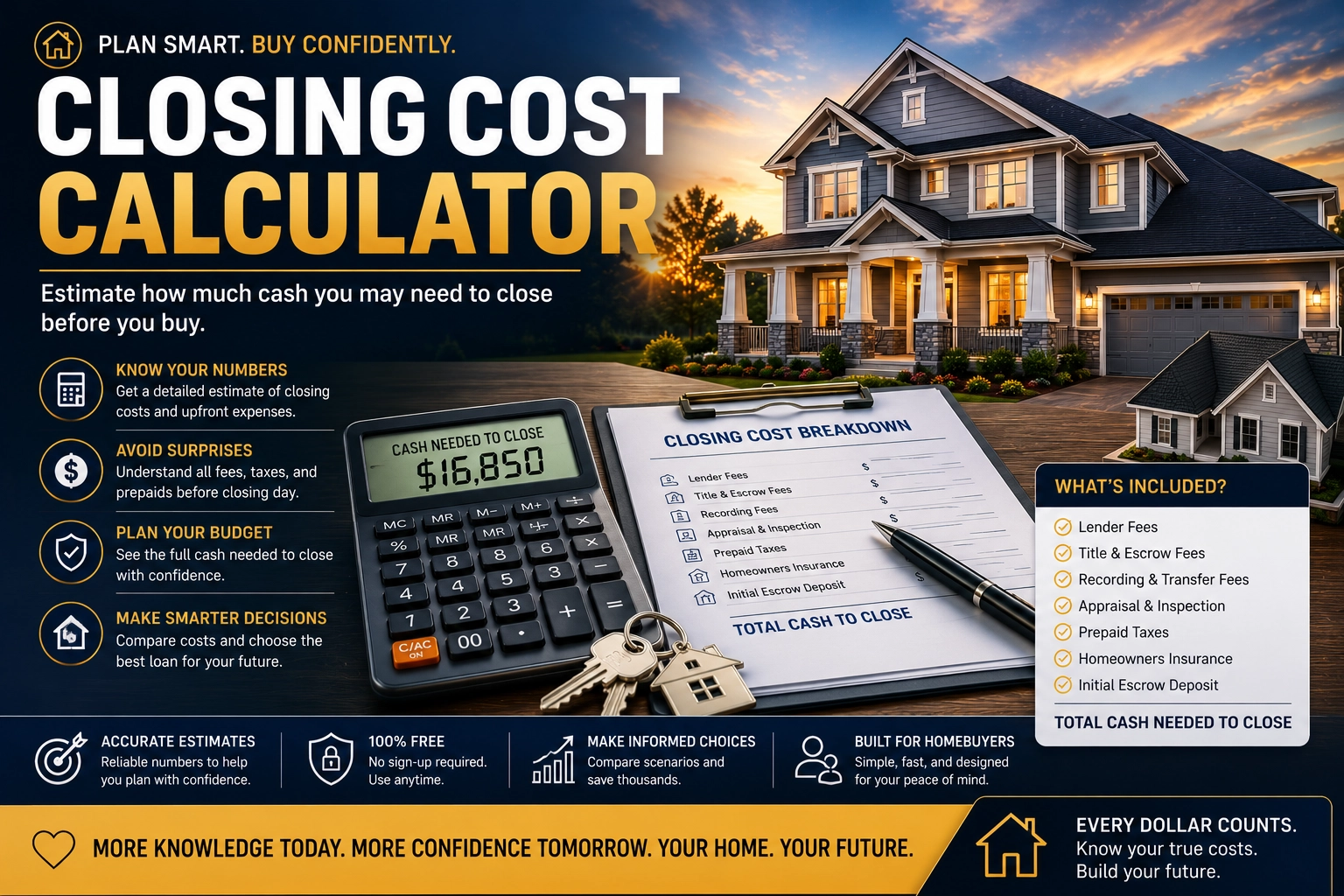

Your Down Payment Isn’t The Only Check You’ll Write.

This calculator estimates the upfront costs buyers may need at closing, including lender fees, title and escrow charges, recording fees, appraisal costs, prepaid taxes, homeowners insurance, escrow deposits, and down payment.

It is designed to help buyers understand the cash needed to close before committing to a home purchase.

Closing Cost Calculator

Estimate your buyer closing costs, prepaid expenses, and cash needed to close.

Purchase Details

Closing Cost Estimates

Prepaid Expenses

Results are estimates and may vary based on lender fees, title company charges, taxes, insurance, escrow requirements, location, and loan type.

FAQ

What are closing costs?

Closing costs are fees and prepaid expenses paid when a real estate transaction is finalized. These may include lender fees, title charges, escrow fees, appraisal costs, prepaid taxes, homeowners insurance, and recording fees.

Are closing costs separate from the down payment?

Yes. The down payment reduces the loan amount, while closing costs are additional expenses required to complete the transaction and transfer ownership.

How much are closing costs on a home purchase?

Closing costs often range between 2% and 5% of the home’s purchase price, although actual costs vary based on lender fees, loan type, taxes, insurance, and local regulations.

What is included in closing costs?

Closing costs may include:

- Lender fees

- Title and escrow fees

- Appraisal and inspection costs

- Recording and transfer fees

- Prepaid property taxes

- Homeowners insurance

- Initial escrow deposits

How much cash do I need to close on a house?

The total cash needed to close usually includes your down payment plus all closing costs and prepaid expenses required by the lender.

Can closing costs be rolled into a mortgage?

In some cases, refinance loans may allow certain closing costs to be rolled into the loan balance. On a purchase loan, many buyers pay closing costs upfront at closing.

Why do lenders require prepaid taxes and insurance?

Lenders often require prepaid taxes and homeowners insurance to establish escrow accounts that help ensure property taxes and insurance premiums are paid on time.

Are closing costs negotiable?

Some lender fees and seller concessions may be negotiable depending on the market, loan type, and terms of the transaction.

Do buyers and sellers both pay closing costs?

Yes. Buyers and sellers may each have their own closing costs depending on the agreement, location, taxes, commissions, and lender requirements.

Why is it important to estimate closing costs early?

Many buyers focus only on the monthly mortgage payment and underestimate the upfront cash required to complete the purchase. Estimating closing costs early can help prevent financial surprises before closing day.

Want To See What The Home May Actually Cost You Monthly?

Use our Mortgage Calculator to estimate monthly payments, taxes, insurance, HOA fees, PMI, total interest paid, and the real long-term cost per square foot — not just the listing price.

Use Mortgage CalculatorExplore Real Estate Listings & Property Values

Research homes, commercial properties, market values, and real estate trends using these popular real estate platforms. Use the mortgage calculator above to compare estimated financing costs before making a purchase decision.